The Statement of Financial Position, previously known as the 'Balance Sheet'.

Liquidity ratios:

The current ratio is a calculation that shows whether a company has enough resources to cover its debts.

Current assets (£'s)

Current liabilities (£'s)

The result is NOT a %.

It is a ratio expressed to 1 ( x:1)

Typically, textbooks will say a ratio of around 2:1 suggest no immediate signs of running out of cash.

More on the current ratio here.

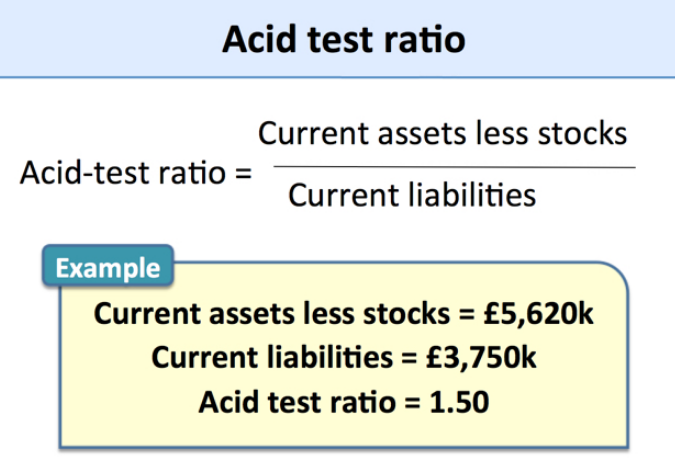

2. Acid Test Ratio

Why is stock (inventory) excluded from current assets?

Typically, textbooks will say a ratio of around 1:1 suggest no immediate signs of running out of cash.

More on the acid test here.

Assessing the value and limitations of ratio analysis. Details here.

You also need to be aware of Working Capital.

A business is solvent if it can meet its short-term debts when they are due for payment.

To do this it needs adequate working capital.

There are three main reasons why a business needs adequate working capital.

It must:

Working capital (£s) = Current assets (£s) minus Current liabilities (£s)

Managing working capital:

Different businesses have different working capital needs.

Larger businesses are likely to have high levels of working capital.

Retailers are going to require higher working capital compared to businesses that do not have much stock.

The typical business needs around twice the amount of current assets to current liabilities to operate safely.

This means its current ratio is close to 2:1.

Maintaining adequate levels of working capital:

If working capital is too little the business will start to encounter problems.

If a business does not have enough stock then manufacturing or sales will stop.

If there is not enough cash in the business, it might not be able to pay bills on time.

On the other hand, a business does not want too much working capital (i.e. current assets are too high and current liabilities are too low.)

Why?

Stocks are costly to keep.

Too much cash is unlikely to be earning high rates of interest and should be being used for more productive purposes.

Ways to improve liquidity:

Liquidity problems can be prevented by keeping a tight control on financial resources.

The use of budgets and cash flow forecasts will improve the financial management of the business.

If a business runs short of cash:

2. Negotiate additional short or long term loans.

3. Encourage cash sales and sell off stocks.

4. Sale and leaseback. An example here.

5. Only make essential payments.

6. Extend credit with selected suppliers.

7. Reduce personal drawings from the business.

8. Introduce fresh capital into the business.

You need to know the consequences of having too little or too much working capital.

More on working capital here.